Updated on March 25th, 2025 by Bob Ciura

Stocks with low P/E ratios can offer attractive returns if their valuation multiples expand.

And when a low P/E stock also has a high dividend yield, investors get ‘paid to wait’ for the valuation multiple to increase.

We define a high-yield stock as one with a current dividend yield of 5% or higher.

The free high dividend stocks list spreadsheet below has our full list of individual securities (stocks, REITs, MLPs, etc.) with with 5%+ dividend yields.

You can download a free copy by clicking on the link below:

In this research report, we discuss the prospects of 20 undervalued high dividend stocks, which are currently trading at P/E ratios under 10 and are offering dividend yields above 5.0%.

International stocks were excluded from this report.

We have ranked the stocks by P/E ratio, from lowest to highest. For REITs, we use P/FFO in place of the P/E ratio. And for MLPs, we use P/DCF (which is distributable cash flows).

These are comparable metrics similar to earnings for common stocks.

These 20 dividend stocks have not been screened for dividend safety. Instead, these are the 20 most undervalued stocks in the Sure Analysis Research Database with high dividend yields.

Table of Contents

- Undervalued High Dividend Stock #1: Shutterstock, Inc. (SSTK)

- Undervalued High Dividend Stock #2: ARMOUR Residential REIT (ARR)

- Undervalued High Dividend Stock #3: AGNC Investment Corporation (AGNC)

- Undervalued High Dividend Stock #4: NewtekOne Inc. (NEWT)

- Undervalued High Dividend Stock #5: Western Union Company (WU)

- Undervalued High Dividend Stock #6: AES Corp. (AES)

- Undervalued High Dividend Stock #7: Ellington Credit Co. (EARN)

- Undervalued High Dividend Stock #8: Sunoco LP (SUN)

- Undervalued High Dividend Stock #9: Macy’s Inc. (M)

- Undervalued High Dividend Stock #10: Virtus Investment Partners (VRTS)

- Undervalued High Dividend Stock #11: Horizon Technology Finance (HRZN)

- Undervalued High Dividend Stock #12: Energy Transfer LP (ET)

- Undervalued High Dividend Stock #13: Ford Motor Co. (F)

- Undervalued High Dividend Stock #14: Canandaigua National Corporation (CNND)

- Undervalued High Dividend Stock #15: Midland States Bancorp (MSBI)

- Undervalued High Dividend Stock #16: Plains All American LP (PAA)

- Undervalued High Dividend Stock #17: Peoples Financial Services (PFIS)

- Undervalued High Dividend Stock #18: Prospect Capital (PSEC)

- Undervalued High Dividend Stock #19: Delek Logistics Partners LP (DLK)

- Undervalued High Dividend Stock #20: Hooker Furnishings Corporation (HOFT)

Keep reading to see analysis on these 20 undervalued high dividend stocks.

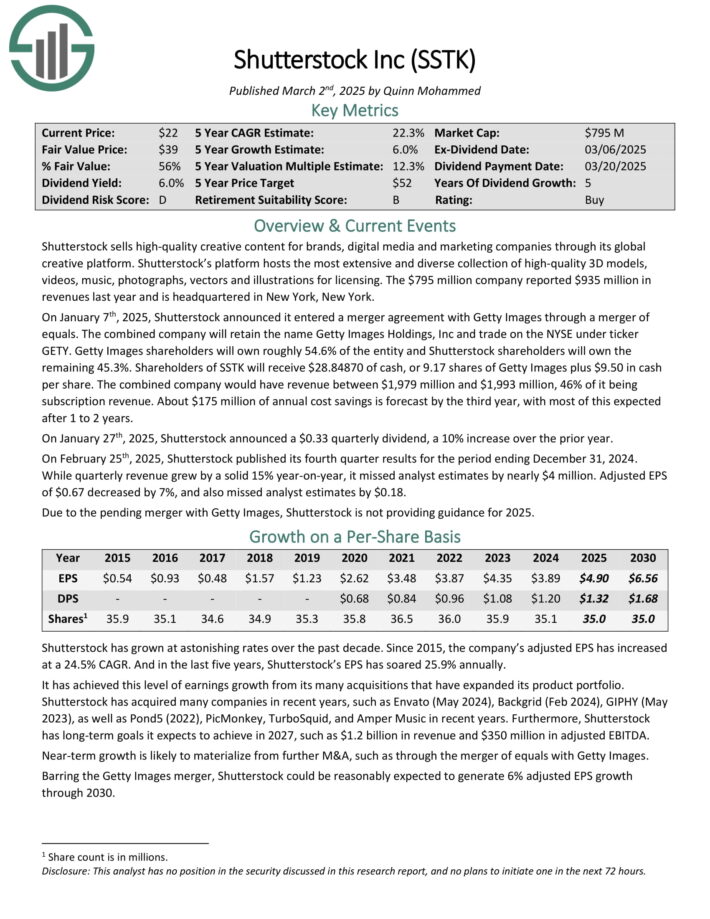

Undervalued High Dividend Stock #1: Shutterstock, Inc. (SSTK) – P/E ratio of 4.0

Shutterstock sells high-quality creative content for brands, digital media and marketing companies through its global creative platform.

Its platform hosts the most extensive and diverse collection of high-quality 3D models, videos, music, photographs, vectors and illustrations for licensing. The company reported $935 million in revenues last year.

On January 7th, 2025, Shutterstock announced it entered a merger agreement with Getty Images through a merger of equals. The combined company will retain the name Getty Images Holdings, Inc and trade on the NYSE under ticker GETY.

Getty Images shareholders will own roughly 54.6% of the entity and Shutterstock shareholders will own the remaining 45.3%. Shareholders of SSTK will receive $28.84870 of cash, or 9.17 shares of Getty Images plus $9.50 in cash per share.

The combined company would have revenue between $1,979 million and $1,993 million, 46% of it being subscription revenue. About $175 million of annual cost savings is forecast by the third year, with most of this expected after 1 to 2 years.

On January 27th, 2025, Shutterstock announced a $0.33 quarterly dividend, a 10% increase over the prior year.

On February 25th, 2025, Shutterstock published its fourth quarter results for the period ending December 31, 2024. While quarterly revenue grew by a solid 15% year-on-year, it missed analyst estimates by nearly $4 million.

Adjusted EPS of $0.67 decreased by 7%, and also missed analyst estimates by $0.18.

Click here to download our most recent Sure Analysis report on SSTK (preview of page 1 of 3 shown below):

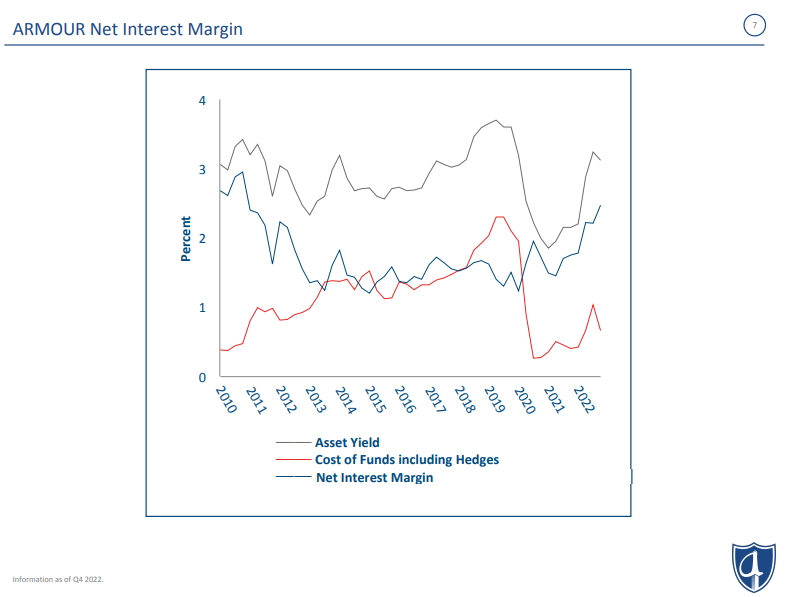

Undervalued High Dividend Stock #2: ARMOUR Residential REIT (ARR) – P/E ratio of 4.4

ARMOUR Residential invests in residential mortgage-backed securities that include U.S. Government-sponsored entities (GSE) such as Fannie Mae and Freddie Mac.

It also includes Ginnie Mae, the Government National Mortgage Administration’s issued or guaranteed securities backed by fixed-rate, hybrid adjustable-rate, and adjustable-rate home loans.

Unsecured notes and bonds issued by the GSE and the US Treasury, money market instruments, and non-GSE or government agency-backed securities are examples of other types of investments.

Source: Investor presentation

On October 23, 2024, ARMOUR Residential REIT announced its unaudited third-quarter 2024 financial results, reporting a GAAP net income available to common stockholders of $62.9 million, or $1.21 per common share. The company generated a net interest income of $1.8 million and distributable earnings of $52.0 million, equivalent to $1.00 per common share.

ARMOUR achieved an average interest income of 4.89% on interest-earning assets and an interest cost of 5.51% on average interest-bearing liabilities. The economic net interest spread stood at 2.00%, calculated from an economic interest income of 4.44% minus an economic interest expense of 2.44%.

During the quarter, ARMOUR raised $129.4 million by issuing 6,413,735 shares of common stock through an at-the-market offering program and paid common stock dividends of $0.72 per share for Q3.

Click here to download our most recent Sure Analysis report on ARMOUR Residential REIT Inc (ARR) (preview of page 1 of 3 shown below):

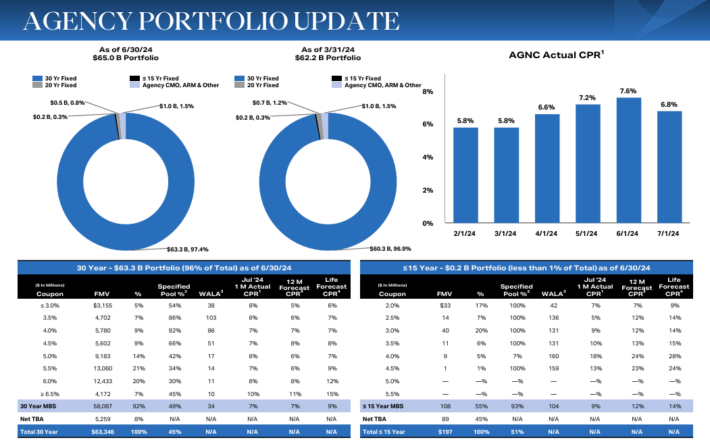

Undervalued High Dividend Stock #3: AGNC Investment Corporation (AGNC) – P/E ratio of 4.5

American Capital Agency Corp is a mortgage real estate investment trust that invests primarily in agency mortgage–backed securities (or MBS) on a leveraged basis.

The firm’s asset portfolio is comprised of residential mortgage pass–through securities, collateralized mortgage obligations (or CMO), and non–agency MBS. Many of these are guaranteed by government–sponsored enterprises.

Source: Investor Presentation

AGNC Investment Corp. reported strong financial results for the third quarter ended September 30, 2024. The company achieved a comprehensive income of $0.63 per common share, driven by a net income of $0.39 and other comprehensive income of $0.24 from marked-to-market investments.

Net spread and dollar roll income contributed $0.43 per share. The tangible net book value increased by $0.42 per share to $8.82, reflecting a 5.0% growth from the previous quarter.

AGNC declared dividends of $0.36 per share, resulting in a 9.3% economic return on tangible common equity, which includes both dividends and the increase in net book value.

Click here to download our most recent Sure Analysis report on AGNC Investment Corp (AGNC) (preview of page 1 of 3 shown below):

Undervalued High Dividend Stock #4: NewtekOne Inc. (NEWT) – P/E ratio of 5.4

Newtek Business Services Corp. was a business development company (BDC) specializing in providing financial and business services to the small- and medium-sized business market in the United States.

What makes NewTek a unique company is that a good portion of its income is derived from subsidiaries that provide a wide array of business services to its large client base.

The company also gets a significant amount of its income from being an issuer of SBA (Small Business Administration loans), which only very few BDCs are licensed to do. This is not your typical BDC that only generates income from interest rate spreads, but also from a much wider range of small business services.

On February 26th, 2025, Newtek released its Q4 and full-year results for the period ending December 31st, 2024. For the quarter, Newtek reported net income of $18.3 million, or diluted earnings per share (EPS) of $0.69, representing a 62.8% increase over the prior year. Net interest income increased to $11.3 million, up 36.1% from Q4 2023.

Its total assets reached $2.1 billion, marking a 50% rise year-over-year, with loans held for investment growing 23% to $991.4 million.

Newtek’s net interest margin was 2.80%, a slight increase from the prior year.

Additionally, the company’s Alternative Loan Program loan closings skyrocketed by 199% to $91.4 million. Newtek also achieved significant improvements in return on tangible common equity (ROTCE) and return on average assets (ROAA), reaching 31.8% and 4.1%.

Click here to download our most recent Sure Analysis report on NEWT (preview of page 1 of 3 shown below):

Undervalued High Dividend Stock #5: Western Union Company (WU) – P/E ratio of 5.8

The Western Union Company is the world leader in the business of domestic and international money transfers. The company has a network of approximately 550,000 agents globally and operates in more than 200 countries.

About 90% of agents are outside of the US. Western Union operates two business segments, Consumer-to-Consumer (C2C) and Other (bill payments in the US and Argentina).

Western Union reported mixed Q4 2024 results on February 4th, 2025. Revenue increased 1% and diluted GAAP earnings per share increased to $1.14 in the quarter, compared to $0.35 in the prior year on higher revenue and a $0.75 tax benefit on reorganizing the international operations.

Revenue rose, despite challenges in Iraq on higher Banded Digital transactions and Consumer Services volumes.

CMT revenue fell 4% year-over-year even with 3% higher transaction volumes. Branded Digital Money Transfer CMT revenues increased 7% as transactions rose 13%. Digital revenue is now 25% of total CMT revenue and 32% of transactions.

Consumer Services revenue rose 56% on new products and expansion of retail foreign exchange offerings. The firm launched a media network business, expanded retail foreign exchange, and grew retail money orders.

Click here to download our most recent Sure Analysis report on WU (preview of page 1 of 3 shown below):

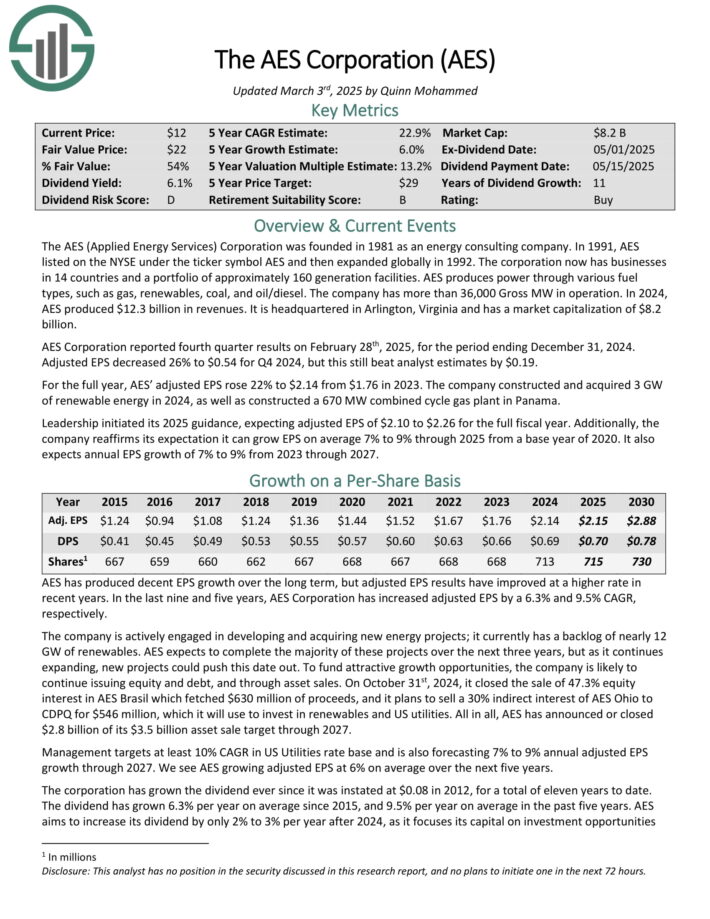

Undervalued High Dividend Stock #6: AES Corp. (AES) – P/E ratio of 5.8

The AES (Applied Energy Services) Corporation was founded in 1981 as an energy consulting company. It now has businesses in 14 countries and a portfolio of approximately 160 generation facilities.

AES produces power through various fuel types, such as gas, renewables, coal, and oil/diesel. The company has more than 36,000 Gross MW in operation.

Source: Investor Presentation

The company is actively engaged in developing and acquiring new energy projects.

It currently has a backlog of 12.7 GW of renewables. AES expects to complete the majority of these projects through 2027.

AES Corporation reported fourth quarter results on February 28th, 2025, for the period ending December 31, 2024. Adjusted EPS decreased 26% to $0.54 for Q4 2024, but this still beat analyst estimates by $0.19.

For the full year, AES’ adjusted EPS rose 22% to $2.14 from $1.76 in 2023. The company constructed and acquired 3 GW of renewable energy in 2024, as well as constructed a 670 MW combined cycle gas plant in Panama.

Leadership initiated its 2025 guidance, expecting adjusted EPS of $2.10 to $2.26 for the full fiscal year.

Additionally, the company reaffirms its expectation it can grow EPS on average 7% to 9% through 2025 from a base year of 2020. It also expects annual EPS growth of 7% to 9% from 2023 through 2027.

Click here to download our most recent Sure Analysis report on AES (preview of page 1 of 3 shown below):

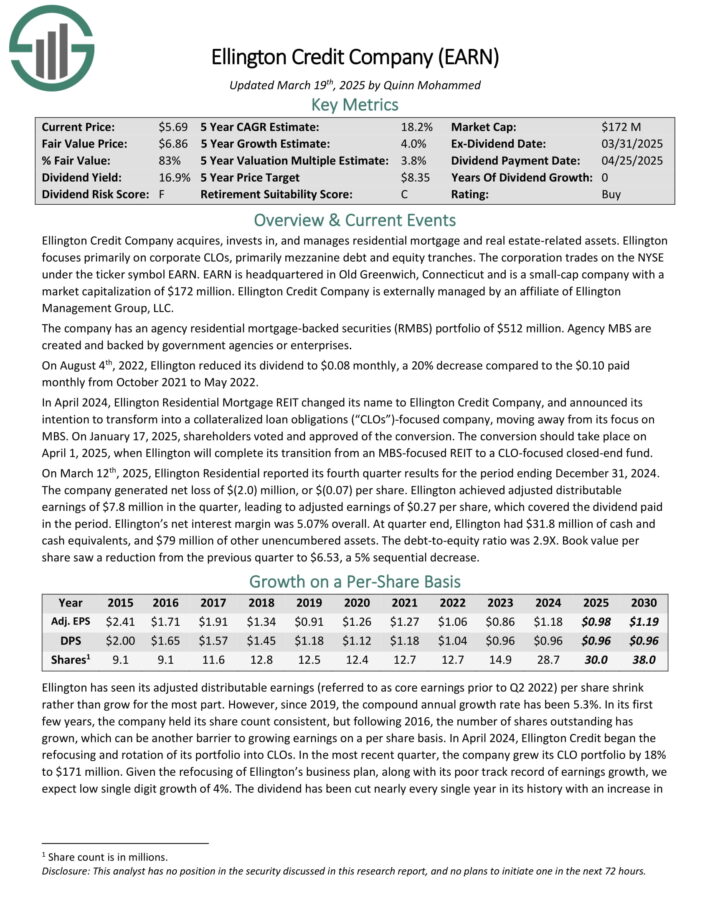

Undervalued High Dividend Stock #7: Ellington Credit Co. (EARN) – P/E ratio of 5.9

Ellington Credit Co. acquires, invests in, and manages residential mortgage and real estate related assets. Ellington focuses primarily on residential mortgage-backed securities, specifically those backed by a U.S. Government agency or U.S. government–sponsored enterprise.

Agency MBS are created and backed by government agencies or enterprises, while non-agency MBS are not guaranteed by the government.

On March 12th, 2025, Ellington Residential reported its fourth quarter results for the period ending December 31, 2024. The company generated a net loss of $(2.0) million, or $(0.07) per share.

Ellington achieved adjusted distributable earnings of $7.8 million in the quarter, leading to adjusted earnings of $0.27 per share, which covered the dividend paid in the period.

Ellington’s net interest margin was 5.07% overall. At quarter end, Ellington had $31.8 million of cash and cash equivalents, and $79 million of other unencumbered assets.

Click here to download our most recent Sure Analysis report on EARN (preview of page 1 of 3 shown below):

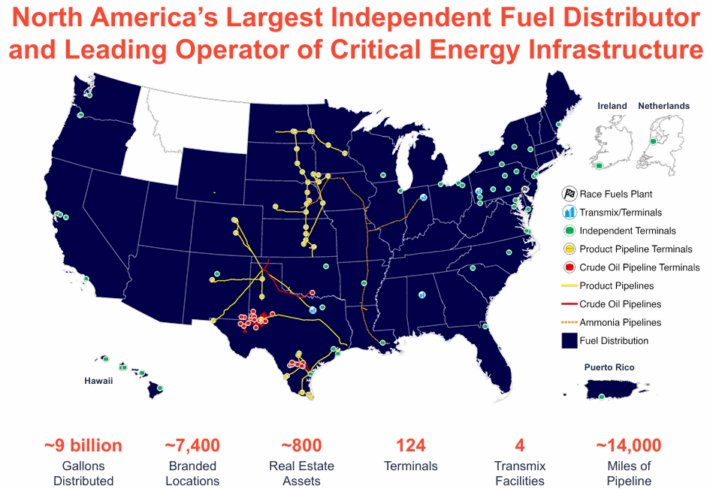

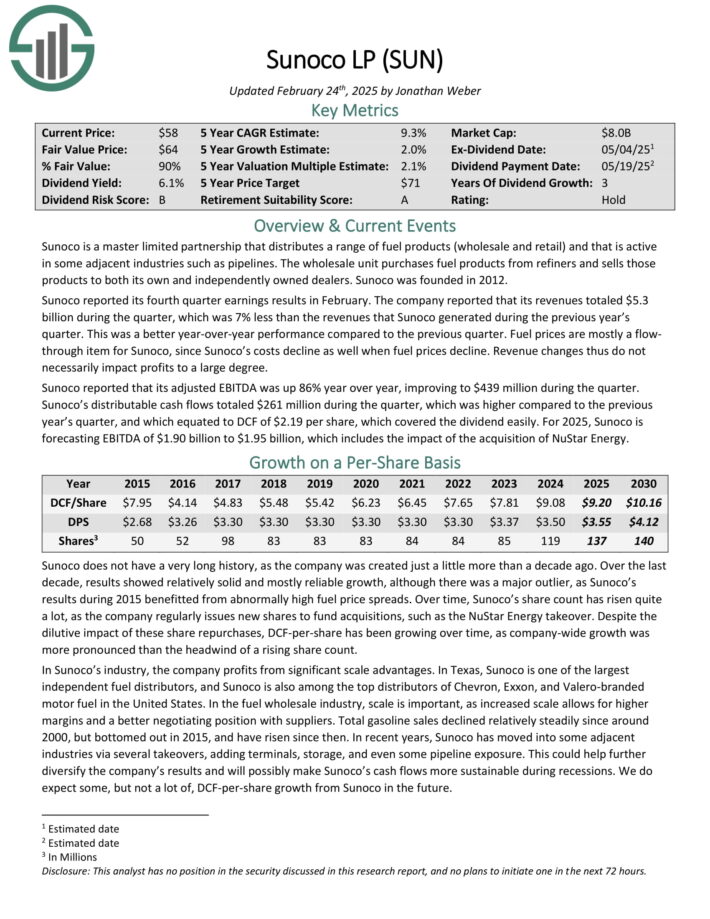

Undervalued High Dividend Stock #8: Sunoco LP (SUN) – P/E ratio of 6.2

Sunoco is a master limited partnership that distributes a range of fuel products (wholesale and retail) and that is active in some adjacent industries such as pipelines.

The wholesale unit purchases fuel products from refiners and sells those products to both its own and independently owned dealers.

Source: Investor Presentation

Sunoco reported its fourth quarter earnings results in February. The company reported that its revenues totaled $5.3 billion during the quarter, which was 7% less than the revenues that Sunoco generated during the previous year’s quarter.

Fuel prices are mostly a flow through item for Sunoco, since Sunoco’s costs decline as well when fuel prices decline. Revenue changes thus do not necessarily impact profits to a large degree.

Sunoco reported that its adjusted EBITDA was up 86% year over year, improving to $439 million during the quarter. Distributable cash flows totaled $261 million during the quarter, which was higher compared to the previous year’s quarter, and which equated to DCF of $2.19 per share.

Click here to download our most recent Sure Analysis report on SUN (preview of page 1 of 3 shown below):

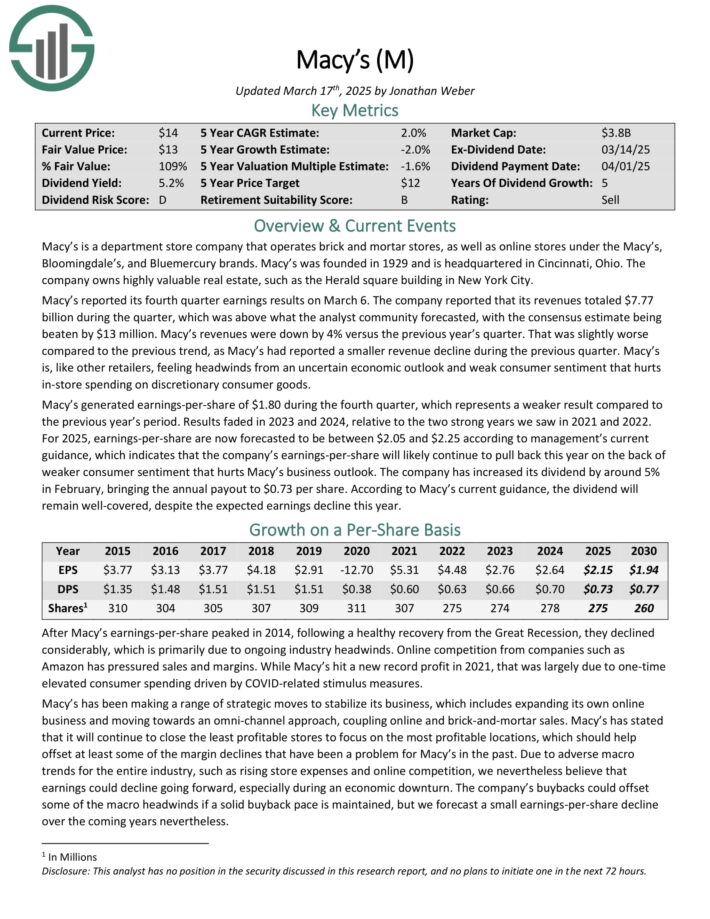

Undervalued High Dividend Stock #9: Macy’s Inc. (M) – P/E ratio of 6.4

Macy’s is a department store company that operates brick and mortar stores, as well as online stores under the Macy’s, Bloomingdale’s, and Bluemercury brands.

Macy’s reported its fourth quarter earnings results on March 6. The company reported that its revenues totaled $7.77 billion during the quarter, which was above what the analyst community forecasted, with the consensus estimate being beaten by $13 million. Macy’s revenues were down by 4% versus the previous year’s quarter.

Macy’s generated earnings-per-share of $1.80 during the fourth quarter, which represents a weaker result compared to the previous year’s period. Results faded in 2023 and 2024, relative to the two strong years we saw in 2021 and 2022.

For 2025, earnings-per-share are now forecasted to be between $2.05 and $2.25 according to management’s current guidance, which indicates that the company’s earnings-per-share will likely continue to pull back this year on the back of weaker consumer sentiment that hurts Macy’s business outlook.

Click here to download our most recent Sure Analysis report on M (preview of page 1 of 3 shown below):

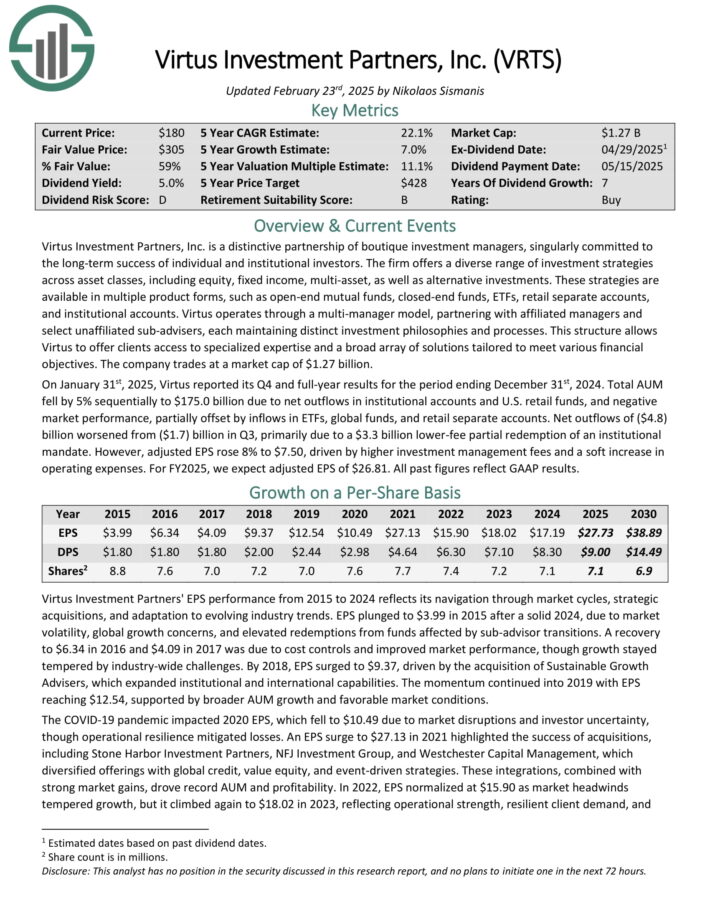

Undervalued High Dividend Stock #10: Virtus Investment Partners (VRTS) – P/E ratio of 6.4

Virtus Investment Partners, Inc. is a distinctive partnership of boutique investment managers, singularly committed to the long-term success of individual and institutional investors.

The firm offers a diverse range of investment strategies across asset classes, including equity, fixed income, multi-asset, as well as alternative investments.

These strategies are available in multiple product forms, such as open-end mutual funds, closed-end funds, ETFs, retail separate accounts, and institutional accounts.

Virtus operates through a multi-manager model, partnering with affiliated managers and select unaffiliated sub-advisers, each maintaining distinct investment philosophies and processes.

This structure allows Virtus to offer clients access to specialized expertise and a broad array of solutions tailored to meet various financial objectives.

On January 31st, 2025, Virtus reported its Q4 and full-year results for the period ending December 31st, 2024. Total AUM fell by 5% sequentially to $175.0 billion due to net outflows in institutional accounts and U.S. retail funds, and negative market performance, partially offset by inflows in ETFs, global funds, and retail separate accounts.

Net outflows of ($4.8) billion worsened from ($1.7) billion in Q3, primarily due to a $3.3 billion lower-fee partial redemption of an institutional mandate.

However, adjusted EPS rose 8% to $7.50, driven by higher investment management fees and a soft increase in operating expenses. For FY2025, we expect adjusted EPS of $26.81.

Click here to download our most recent Sure Analysis report on VRTS (preview of page 1 of 3 shown below):

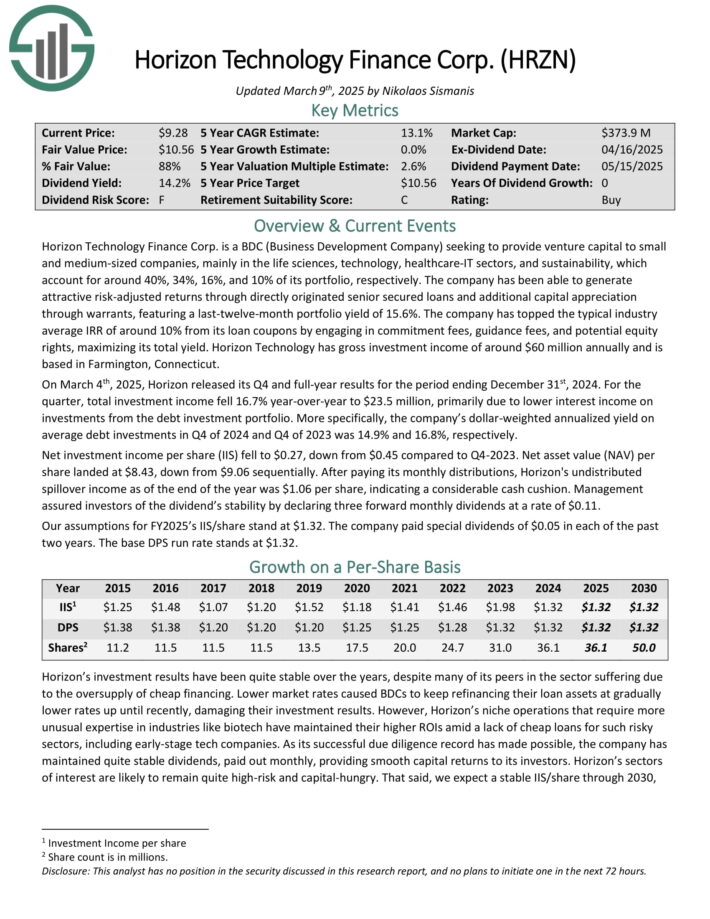

Undervalued High Dividend Stock #11: Horizon Technology Finance (HRZN) – P/E ratio of 7.0

Horizon Technology Finance Corp. is a BDC that provides venture capital to small and medium–sized companies in the technology, life sciences, and healthcare–IT sectors.

The company has generated attractive risk–adjusted returns through directly originated senior secured loans and additional capital appreciation through warrants.

Source: Investor Presentation

On March 4th, 2025, Horizon released its Q4 and full-year results for the period ending December 31st, 2024. For the quarter, total investment income fell 16.7% year-over-year to $23.5 million, primarily due to lower interest income on investments from the debt investment portfolio.

More specifically, the company’s dollar-weighted annualized yield on average debt investments in Q4 of 2024 and Q4 of 2023 was 14.9% and 16.8%, respectively.

Net investment income per share (IIS) fell to $0.27, down from $0.45 compared to Q4-2023. Net asset value (NAV) per share landed at $8.43, down from $9.06 sequentially.

Click here to download our most recent Sure Analysis report on HRZN (preview of page 1 of 3 shown below):

Undervalued High Dividend Stock #12: Energy Transfer LP (ET) – P/E ratio of 7.0

Energy Transfer owns and operates one of the largest and most diversified portfolios of energy assets in the United States.

Operations include natural gas transportation and storage along with crude oil, natural gas liquids, refined product transportation, and storage totaling 83,000 miles of pipelines.

Energy Transfer operates with a primarily fee-based model, which somewhat mitigates the sensitivity of the MLP to commodity prices.

In mid-February, Energy Transfer reported (2/11/25) financial results for the fourth quarter of fiscal 2024. The MLP continued to grow its volumes in all the segments. As a result, adjusted EBITDA grew 8% over the prior year’s quarter.

Energy Transfer maintained a healthy distribution coverage ratio of 1.8 and raised the quarterly distribution by 0.8%, on top of the distribution hikes in each of the twelve previous quarters.

Thanks to strong growth in the demand for its networks, Energy Transfer provided positive guidance for 2025, expecting adjusted EBITDA $16.1 to $16.5 billion. This guidance implies 5% growth at the mid-point.

Click here to download our most recent Sure Analysis report on ET (preview of page 1 of 3 shown below):

Undervalued High Dividend Stock #13: Ford Motor Company (F) – P/E ratio of 7.2

Ford Motor Company was first incorporated in 1903 and in the past 120 years, it has become one of the world’s largest automakers. It operates a large financing business as well as its core manufacturing division, which produces a popular assortment of cars, trucks, and SUVs.

Ford posted fourth quarter and full-year earnings on February 5th, 2025, and results were better than expected. Adjusted earnings-per-share came to 39 cents, which was seven cents ahead of estimates.

Revenue was up almost 5% year-over-year for the quarter to $48.2 billion, which also beat estimates by $5.37 billion. The fourth quarter was the highest revenue total the company has ever produced.

Ford Blue increased 4.2% to $27.3 billion in revenue for the fourth quarter, beating estimates of $25.9 billion. Model e revenue was down 13% year-over-year to $1.4 billion, $400 million less than expected.

Ford Pro revenue was up 5.3% to $16.2 billion, beating estimates for $15.6 billion.

For this year, Ford expects full-year adjusted EBIT of $7 to $8.5 billion, and for adjusted free cash flow of $3.5 billion to $4.5 billion, with capex of $8 to $9.5 billion.

Click here to download our most recent Sure Analysis report on Ford (preview of page 1 of 3 shown below):

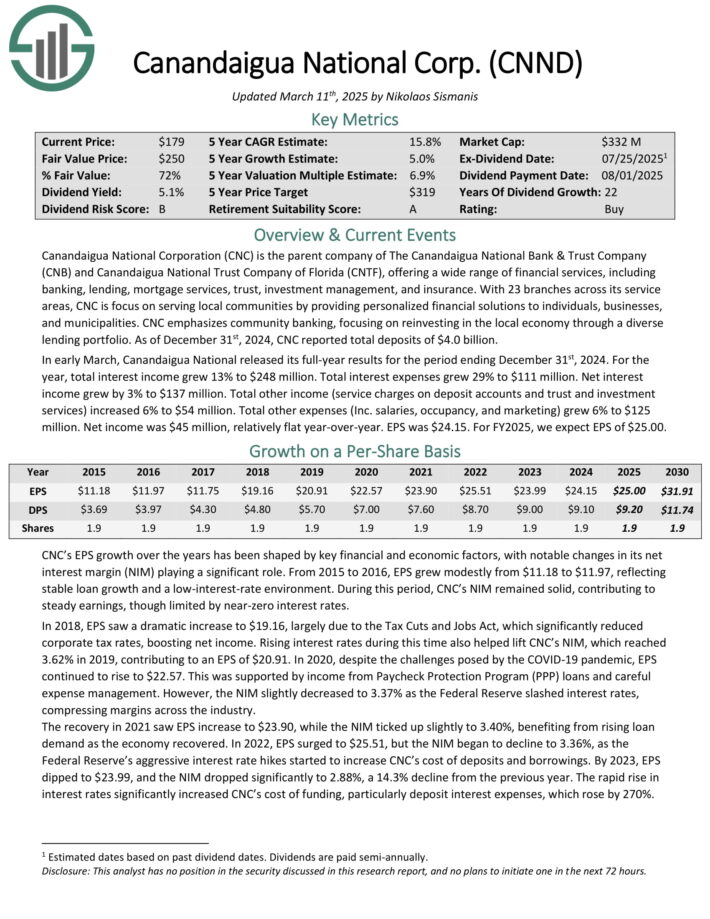

Undervalued High Dividend Stock #14: Canandaigua National Corporation (CNND) – P/E ratio of 7.2

Canandaigua National Corporation (CNC) is the parent company of The Canandaigua National Bank & Trust Company (CNB) and Canandaigua National Trust Company of Florida (CNTF).

The company offers a wide range of financial services, including banking, lending, mortgage services, trust, investment management, and insurance.

With 23 branches across its service areas, CNC is focus on serving local communities by providing personalized financial solutions to individuals, businesses, and municipalities. CNC emphasizes community banking, focusing on reinvesting in the local economy through a diverse lending portfolio.

Moving forward, we expect CNC’s EPS to grow at a CAGR of 5%. Note that the company has increased its dividend every year since 2002, marking 22 years of consecutive annual dividend increases.

Click here to download our most recent Sure Analysis report on CNND (preview of page 1 of 3 shown below):

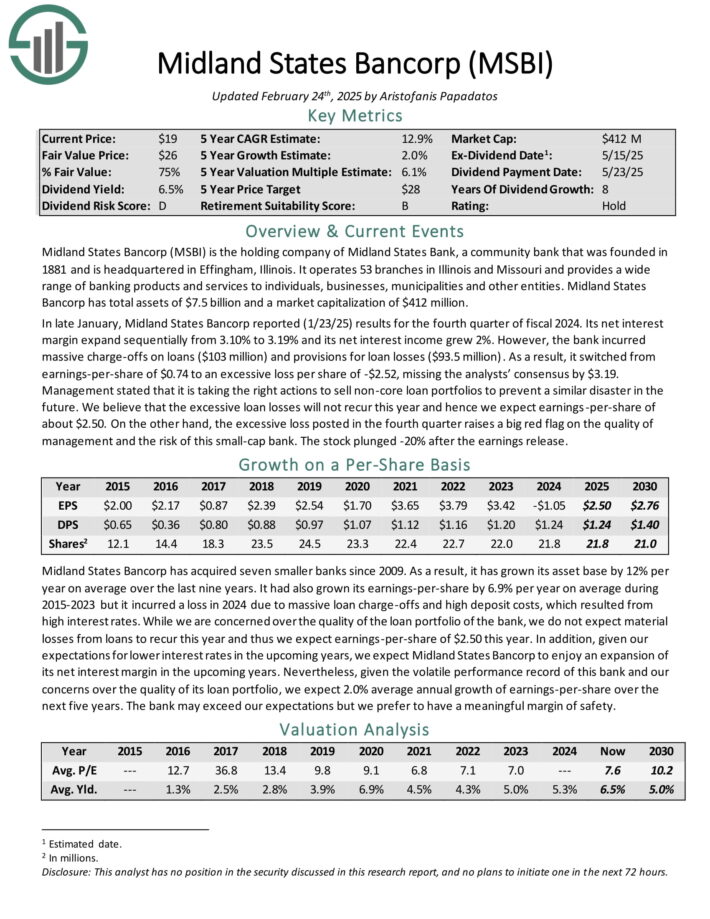

Undervalued High Dividend Stock #15: Midland States Bancorp (MSBI) – P/E ratio of 7.2

Midland States Bancorp (MSBI) is the holding company of Midland States Bank, a community bank that was founded in 1881 and is headquartered in Effingham, Illinois.

It operates 53 branches in Illinois and Missouri and provides a wide range of banking products and services to individuals, businesses, municipalities and other entities. Midland States Bancorp has total assets of $7.5 billion.

In late January, Midland States Bancorp reported (1/23/25) results for the fourth quarter of fiscal 2024. Its net interest margin expand sequentially from 3.10% to 3.19% and its net interest income grew 2%.

However, the bank incurred massive charge-offs on loans ($103 million) and provisions for loan losses ($93.5 million).

As a result, it switched from earnings-per-share of $0.74 to an excessive loss per share of -$2.52, missing the analysts’ consensus by $3.19.

Midland States Bancorp has acquired seven smaller banks since 2009. As a result, it grew its asset base by 12% per year on average over the last nine years.

It had also grown its earnings-per-share by 6.9% per year on average during 2015-2023 but it incurred a loss in 2024 due to massive loan charge-offs and high deposit costs, which resulted from high interest rates.

Click here to download our most recent Sure Analysis report on MSBI (preview of page 1 of 3 shown below):

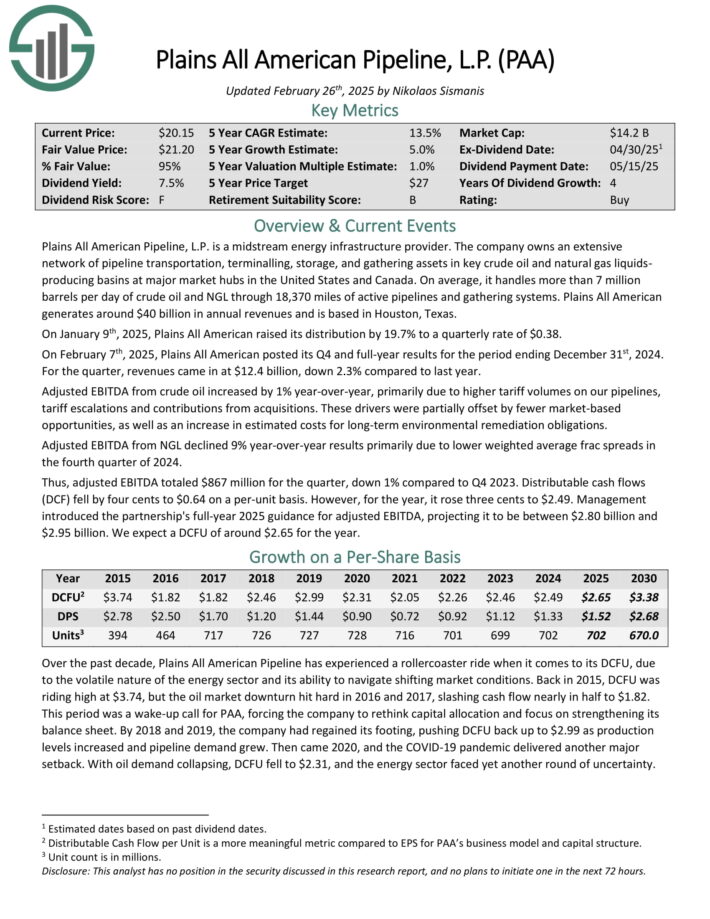

Undervalued High Dividend Stock #16: Plains All American LP (PAA) – P/E ratio of 7.6

Plains All American Pipeline, L.P. is a midstream energy infrastructure provider. The company owns an extensive network of pipeline transportation, terminaling, storage, and gathering assets in key crude oil and natural gas liquids-producing basins at major market hubs in the United States and Canada.

Source: Investor Presentation

On February 7th, 2025, Plains All American posted its Q4 and full-year results for the period ending December 31st, 2024.

For the quarter, revenues came in at $12.4 billion, down 2.3% compared to last year. Adjusted EBITDA from crude oil increased by 1% year-over-year, primarily due to higher tariff volumes on its pipelines, tariff escalations and contributions from acquisitions.

Adjusted EBITDA from NGL declined 9% year-over-year results primarily due to lower weighted average frac spreads in the fourth quarter of 2024.

Click here to download our most recent Sure Analysis report on PAA (preview of page 1 of 3 shown below):

Undervalued High Dividend Stock #17: Peoples Financial Services (PFIS) – P/E ratio of 7.8

Peoples Financial Services (PFIS) is the holding company of Peoples Security Bank and Trust Company, a community bank that was founded in 1905 and is headquartered in Scranton, Pennsylvania.

It operates 44 branches in Pennsylvania and provides various banking products and services to consumers, municipalities and businesses.

On July 1st, 2024, Peoples Financial Services completed its acquisition of FNCB Bancorp in an all-stock deal. As per the terms of the deal, the shareholders of FNCB now own ~29% of the combined entity.

Thanks to the merger, the bank grew its total assets from $3.7 billion to $5.5 billion and thus it became the 5th largest community bank in Pennsylvania.

In early February, Peoples Financial Services reported (2/6/24) financial results for the fourth quarter of fiscal 2024. Loans and deposits grew 40% and 28%, respectively, over the prior year’s quarter, thanks to the acquisition of FNCB Bancorp.

Net interest margin expanded impressively, from 2.30% in the prior year’s quarter to 3.25% thanks to the much higher net interest margin of the acquired bank.

Click here to download our most recent Sure Analysis report on PFIS (preview of page 1 of 3 shown below):

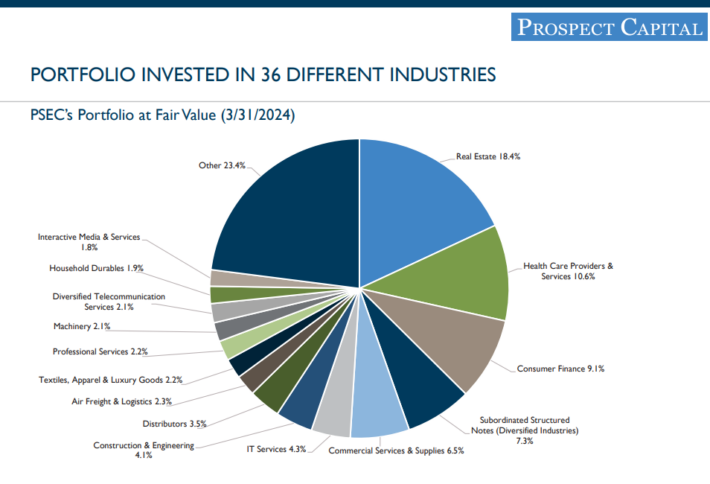

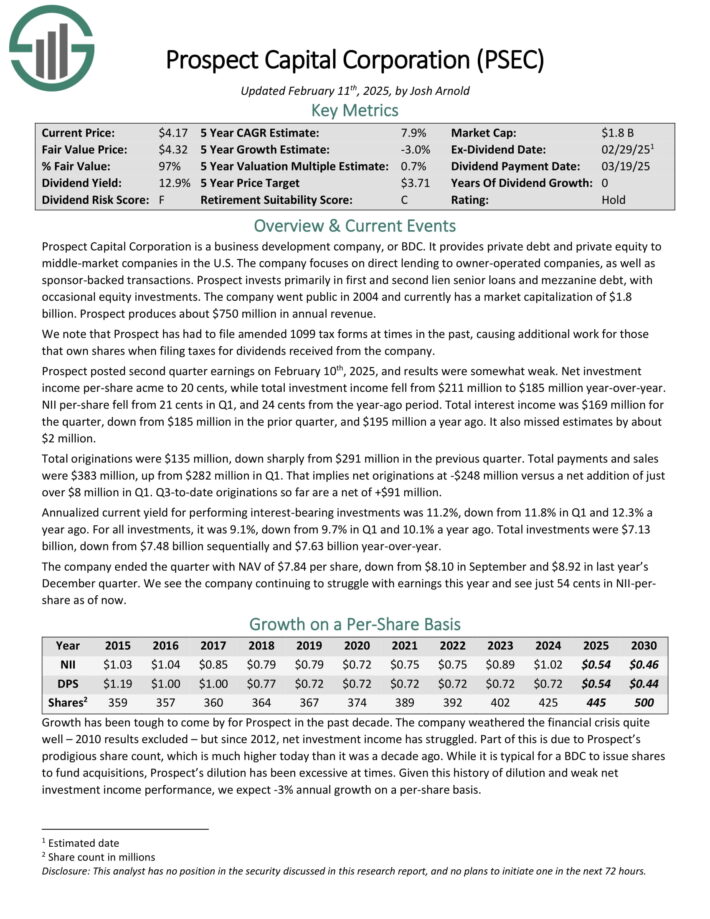

Undervalued High Dividend Stock #18: Prospect Capital (PSEC) – P/E ratio of 7.9

Prospect Capital Corporation is a Business Development Company, or BDC, that provides private debt and private equity to middle–market companies in the U.S.

The company focuses on direct lending to owner–operated companies, as well as sponsor–backed transactions. Prospect invests primarily in first and second lien senior loans and mezzanine debt, with occasional equity investments.

Source: Investor Presentation

Prospect posted second quarter earnings on February 10th, 2025, and results were somewhat weak. Net investment income per-share acme to 20 cents, while total investment income fell from $211 million to $185 million year-over-year.

NII per-share fell from 21 cents in Q1, and 24 cents from the year-ago period. Total interest income was $169 million for the quarter, down from $185 million in the prior quarter, and $195 million a year ago. It also missed estimates by about $2 million.

Click here to download our most recent Sure Analysis report on PSEC (preview of page 1 of 3 shown below):

Undervalued High Dividend Stock #19: Delek Logistics Partners LP (DLK) – P/E ratio of 7.9

Delek Logistics Partners, LP is a publicly traded master limited partnership (MLP) headquartered in Brentwood, Tennessee.

Established in 2012 by Delek US Holdings, Inc. (NYSE: DK), Delek Logistics owns and operates a network of midstream energy infrastructure assets.

These assets include approximately 850 miles of crude oil and refined product transportation pipelines and a 700-mile crude oil gathering system, primarily located in the southeastern United States and west Texas.

The company’s operations are integral to Delek US’s refining activities, particularly supporting refineries in Tyler, Texas, and El Dorado, Arkansas.

Delek Logistics provides services such as gathering, transporting, and storing crude oil, as well as marketing, distributing, and storing refined products for both Delek US and third-party customers.

On February 25, 2025, Delek Logistics Partners (DKL) reported its financial results for the fourth quarter of 2024. The company achieved an adjusted EBITDA of approximately $107.2 million, an increase from $100.9 million in the same period of the previous year.

Distributable cash flow was $69.5 million, with a coverage ratio of approximately 1.2 times. The Gathering and Processing segment saw an adjusted EBITDA of $66 million, up from $53.3 million in Q4 2023, primarily due to higher throughput from Permian Basin assets and contributions from the H2O Midstream acquisition.

Click here to download our most recent Sure Analysis report on DKL (preview of page 1 of 3 shown below):

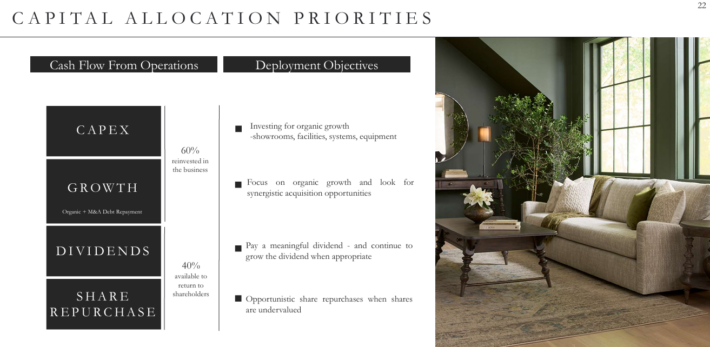

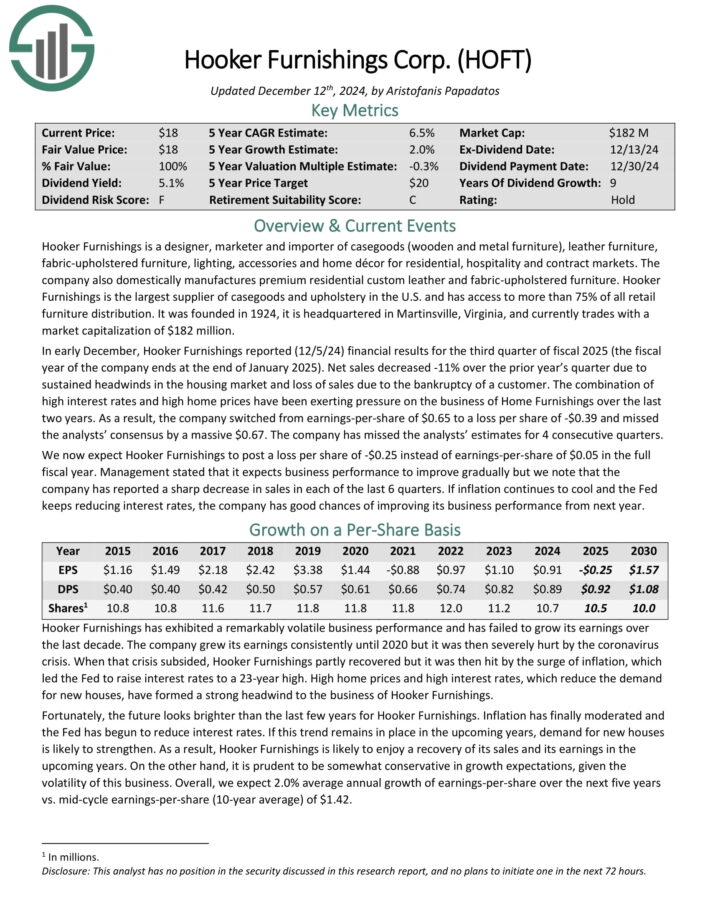

Undervalued High Dividend Stock #20: Hooker Furnishings Corporation (HOFT) – P/E ratio of 7.9

Hooker Furnishings is a designer, marketer and importer of casegoods (wooden and metal furniture), leather furniture, fabric-upholstered furniture, lighting, accessories and home décor for residential, hospitality and contract markets.

The company also domestically manufactures premium residential custom leather and fabric-upholstered furniture.

Hooker Furnishings is the largest supplier of casegoods and upholstery in the U.S. and has access to more than 75% of all retail furniture distribution.

Source: Investor Presentation

In early December, Hooker Furnishings reported (12/5/24) financial results for the third quarter of fiscal 2025. Net sales decreased -11% over the prior year’s quarter due to sustained headwinds in the housing market and loss of sales due to the bankruptcy of a customer.

The combination of high interest rates and high home prices have been exerting pressure on the business of Home Furnishings over the last two years.

As a result, the company switched from earnings-per-share of $0.65 to a loss per share of -$0.39 and missed the analysts’ consensus by a massive $0.67.

Click here to download our most recent Sure Analysis report on HOFT (preview of page 1 of 3 shown below):

Final Thoughts

All the above stocks are trading at remarkably cheap valuation levels due to some business headwinds. Some of them have been hurt by high inflation or the latest economic slowdown whereas others are facing their own specific issues.

Moreover, all the above stocks are offering dividend yields above 5%. As a result, they make it much easier for investors to wait patiently for the business headwinds to subside.

If you are interested in finding high-quality dividend growth stocks and/or other high-yield securities and income securities, the following Sure Dividend resources will be useful:

High-Yield Individual Security Research

- 20 Highest-Yielding BDCs

- 20 Highest-Yielding MLPs

- 20 Best Ultra High-Dividend Stocks

- 20 High-Dividend Stocks Under $10

- 20 Highest-Yielding Dividend Aristocrats

- 20 Highest Yielding Monthly Dividend Stocks

- 20 Highest-Yielding Small Cap Dividend Stocks

- 20 Safe High Dividend Blue-Chip Stocks With Low Volatility

- 10 Super High Dividend REITs

- 4 Highest Yielding Royalty Trusts

Other Sure Dividend Resources

- Dividend Kings: 50+ years of rising dividends

- Dividend Champions: 25+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Dividend Achievers: 10+ years of rising dividends and in the NASDAQ

- Monthly Dividend Stocks: Individual securities that pay out every month

- Blue Chip Stock: Kings, Aristocrats, and Achievers

- MLPs: List of MLPs and more

- REITs: List of REITs and more

- BDCs: List of BDCs and more