Updated on September 6st, 2024 by Felix Martinez

ARMOUR Residential REIT Inc. (ARR) is a mortgage Real Estate Investment Trust (mREIT) that offers an appealing 14.2% dividend yield, making it a high dividend stock.

ARMOUR Residential also pays its dividends on a monthly basis, which is rare as the vast majority of companies that pay a dividend, pay them quarterly or semi-annually.

There are currently over 78 monthly dividend stocks in our coverage universe. You can download our full list of monthly dividend stocks (along with price-to-earnings ratios, dividend yields, and payout ratios) by clicking on the link below:

ARMOUR Residential’s high dividend yield and monthly dividend payments make it an intriguing stock for dividend investors, even though its dividend payments have been declining over the years.

As with many high-dividend stocks yielding over 10%, the sustainability of the dividend is in question. This article will analyze the investment prospects of ARMOUR Residential.

Business Overview

As an mREIT, ARMOUR Residential invests in residential mortgage-backed securities that include U.S. Government-sponsored entities (GSE) such as Fannie Mae, Freddie Mac. It also includes Ginnie Mae, the Government National Mortgage Administration’s issued or guaranteed securities backed by fixed-rate, hybrid adjustable-rate, and adjustable-rate home loans.

It also includes unsecured notes and bonds issued by the GSE and the United States treasuries, money market instruments, and non-GSE or government agency-backed securities.

The mortgage REIT was founded in 2008 and is based in Vero Beach, Florida. It seeks to create shareholder value through careful investment and risk management practices that produce current yield and superior risk-adjusted returns over the long term.

With a market cap of approximately $1 billion and ~$107.6 million in annual revenue, it is a significant national player in residential investment.

Source: Investor presentation

The trust makes money by raising capital through issuing debt as well as preferred and common equity and then reinvesting the proceeds into higher-yielding debt instruments.

The spread (i.e., the difference between the cost of capital and the return on capital) is then largely returned to common shareholders via dividend payments, though the trust often retains a little bit of the profits to reinvest in the business.

Growth Prospects

Recent results at ARMOUR have been mixed. The trust was severely impacted by the COVID-19 pandemic, but was able to meet all of its margin calls and it maintained access to repurchase financing.

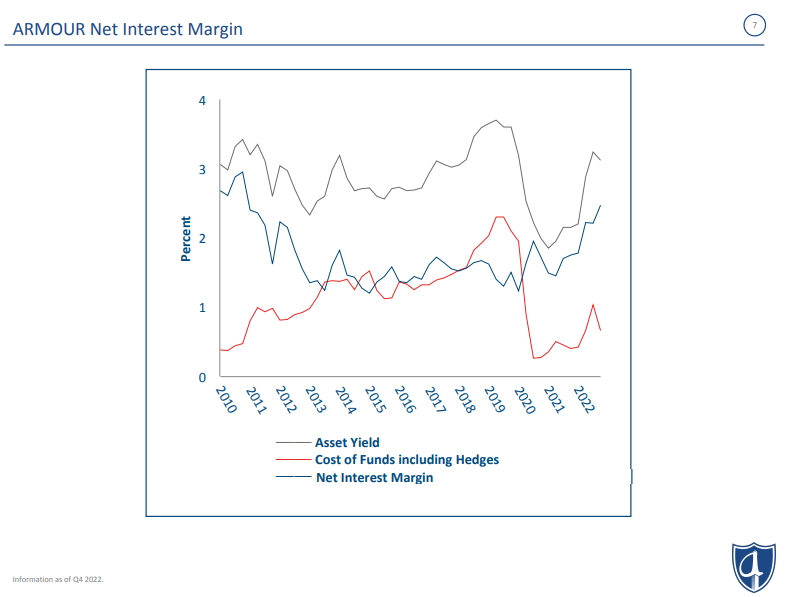

ARMOUR Residential REIT, Inc. (ARR) reported its unaudited second-quarter 2024 financial results and financial position as of June 30, 2024. The company reported a GAAP net loss of $51.3 million or $1.05 per share for common stockholders. However, distributable earnings for the quarter were $52.5 million, equivalent to $1.08 per common share. The company paid dividends of $0.24 per common share each month, totaling $0.72 for the quarter. ARMOUR’s economic net interest spread was 2.05%, with average interest income at 5.00% and average interest expense at 5.52%.

As of June 30, 2024, ARMOUR’s book value per common share stood at $20.30, down from $22.07 on March 31, 2024, reflecting the quarter’s net loss and dividends. The company’s liquidity was strong, with $630.2 million in cash and unencumbered securities. ARMOUR’s agency mortgage-backed securities (MBS) portfolio amounted to $8.9 billion, and its repurchase agreements totaled $7.1 billion. The company’s debt-to-equity ratio was 6.09:1, and including TBA Securities, its implied leverage reached 7.44:1.

In a company update, as of July 22, 2024, ARMOUR had 48.8 million common shares outstanding and an estimated book value per share of $20.37. Liquidity was over $553 million, with additional MBS receivables of $98.1 million. The total securities portfolio was valued at $10.4 billion. ARMOUR’s debt-to-equity ratio increased slightly to 6.5:1, with implied leverage rising to 7.8:1. The company also processed the dismissal of the JAVELIN Mortgage Investment Corp. shareholder litigation appeal in July 2024.

Source: Investor presentation

ARMOUR’s cash flow has been volatile since its inception in 2008, but this is to be expected with all mREITs. Of late, declining spreads have hurt earnings while the economic disruption caused by the coronavirus outbreak disrupted the business model, leading to a sharp decline in cash flow per share, as well as a steep dividend cut. Fortunately, ARMOUR is now seeing a measure of recovery, and should continue to see that recovery manifest itself in the coming quarters and years. Moving forward, we expect the company to grow slowly, though it will likely take a long time for them to rebuild to previous levels of book value and earnings power.

Risk Considerations

While there have certainly been some positive developments at work for ARMOUR, there are still several risks to be concerned about. ARMOUR’s quality metrics have been volatile given the performance of the trust as rates have moved around over the years. Gross margins have moved down since short–term rates began to rise meaningfully a couple of years ago, although it appears most of that damage has been done.

Balance sheet leverage had been moving down slightly, but it saw an uptick again this past quarter. However, we do not forecast a significant movement in either direction from this point. Interest coverage has declined with spreads but also appears to have stabilized, so we are somewhat optimistic moving forward while keeping in mind the significant potential for volatility.

ARMOUR was facing headwinds from the coronavirus outbreak and an overall economic downturn. As a result, a steep dividend cut was necessary to preserve the balance sheet and allow the REIT to reposition itself for survival and future growth.

The annualized dividend payout of $2.88 per share will represent 75% of the company’s EPS (we estimate 2024 EPS of $4.18). This is a concern as the payout ratio is high, and the dividend could be at risk of further reduction if EPS falls or stays at this level for too long.

For example, if the economy were to go into recession, mortgage defaults could surge, leading to steep losses. Given the uncertain macroeconomic outlook, this risk is relevant for investors.

Final Thoughts

ARMOUR Residential’s high dividend yield and monthly dividend payments make it stand out to high-yield dividend investors. However, we remain cautious on the stock especially in light of the multiple dividend cuts in recent years.

While the trust is able to cover its dividend currently, declining interest rates could continue to force the trust ever further out on the risk spectrum to maintain its cash flows as its older mortgages roll off the balance sheet. This sets it up for potentially steep losses if the economy were to slip into a recession.

Therefore, ARMOUR stock carries notably higher levels of risk. This makes the investment highly speculative right now, especially for risk-averse income investors such as retirees. As a result, we encourage risk-averse investors to look elsewhere for sustainable and growing income.

Don’t miss the resources below for more monthly dividend stock investing research.

- The Monthly Dividend Stocks List

- 20 Highest Yielding Monthly Dividend Stocks

- 10 Cheapest Monthly Dividend Stocks

- 10 Safest Monthly Dividend Stocks

- 3 Top ‘Hold Forever’ Monthly Dividend Stocks

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

- Dividend Kings: 50+ years of rising dividends

- Dividend Champions: 25+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Dividend Achievers: 10+ years of rising dividends and in the NASDAQ

- High Dividend Stocks: 4%+ dividend yields

- Blue Chip Stock: Kings, Aristocrats, and Achievers

- MLPs: List of MLPs and more

- REITs: List of REITs and more

- BDCs: List of BDCs and more