Updated on October 8th, 2024 by Bob Ciura

Investors looking to generate higher income levels from their investment portfolios should look at Real Estate Investment Trusts or REITs.

These are companies that own real estate properties and lease them to tenants, or invest in real estate backed loans, both of which generate a steady stream of income.

The bulk of their income is then passed on to shareholders through dividends. You can see all 200+ REITs here.

You can download our full list of REITs, along with important metrics such as dividend yields and market capitalizations, by clicking on the link below:

The beauty of REITs for income investors is that they are required to distribute 90% of their taxable income to shareholders annually in the form of dividends. In return, REITs typically do not pay corporate taxes.

As a result, many of the 200+ REITs we track offer high dividend yields of 5%+.

But not all high-yielding stocks are automatic buys. Investors should carefully assess the fundamentals to ensure that high yields are sustainable.

Note that while the securities in this article have very high yields, a high yield alone does not make for a solid investment. Dividend safety, valuation, management, balance sheet health, and growth are also very important factors.

We urge investors to use the analysis below as informative but to do significant due diligence before buying into any security – especially high-yield securities.

Many (but not all) high-yield securities have a significant risk of a dividend reduction and/or deteriorating business results.

Table of Contents

You can instantly jump to any specific section of the article by using the links below:

- High-Yield REIT No. 10: Global Net Lease (GNL)

- High-Yield REIT No. 9: Sachem Capital (SACH)

- High-Yield REIT No. 8: Annaly Capital (NLY)

- High-Yield REIT No. 7: New York Mortgage REIT (NYMT)

- High-Yield REIT No. 6: Two Harbors Investment Corp. (TWO)

- High-Yield REIT No. 5: Ares Commercial Real Estate (ACRE)

- High-Yield REIT No. 4: AGNC Investment Corp. (AGNC)

- High-Yield REIT No. 3: Ellington Credit Co. (EARN)

- High-Yield REIT No. 2: ARMOUR Residential REIT (ARR)

- High-Yield REIT No. 1: Orchid Island Capital (ORC)

High-Yield REIT No. 10: Global Net Lease (GNL)

- Dividend Yield: 13.1%

Global Net Lease invests in commercial properties in the U.S. and Europe with an emphasis on sale-leaseback transactions. GNL’s portfolio includes over 1300 properties, spanning nearly 67 million square feet with a gross asset value of $9.2 billion.

On August 6, 2024, Global Net Lease reported its financial results for the second quarter of 2024. The company recorded a net loss per share of $0.20, missing expectations by $0.05. Revenue for the quarter was $203.29 million, which, despite representing a significant 112.10% year-over-year increase, missed estimates by $2.06 million.

During the quarter, GNL increased its Adjusted Funds from Operations (AFFO) per share by 2% to $0.33, while reducing its outstanding debt by $251 million. This debt reduction improved the company’s Net Debt to Adjusted EBITDA ratio from 8.4x to 8.1x.

Click here to download our most recent Sure Analysis report on Global Net Lease (GNL) (preview of page 1 of 3 shown below):

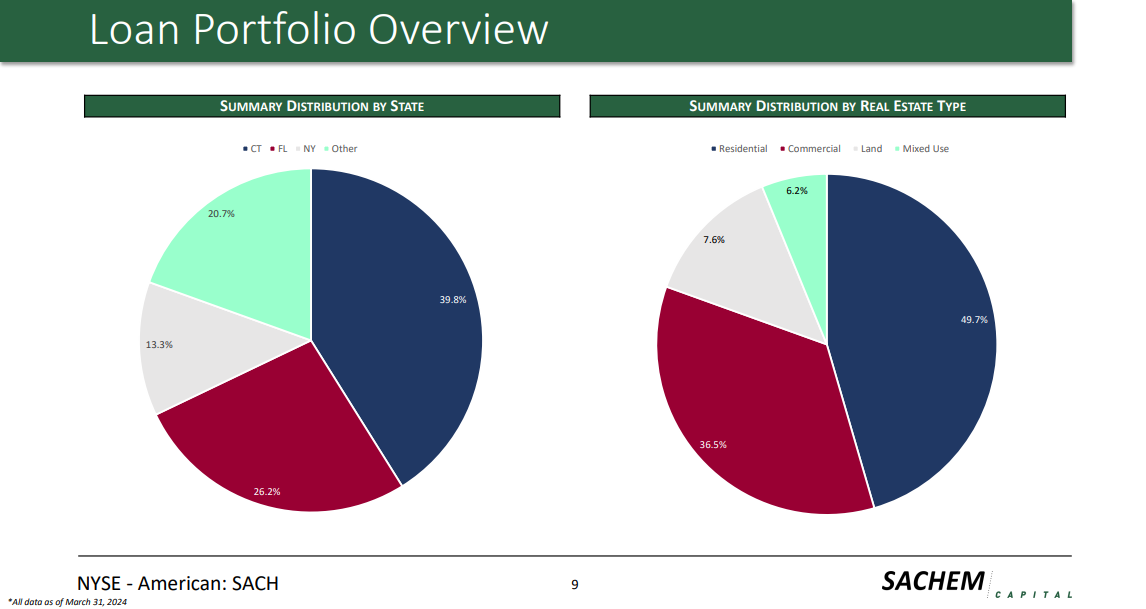

High-Yield REIT No. 9: Sachem Capital (SACH)

- Dividend Yield: 13.3%

Sachem Capital Corp is a Connecticut-based real estate finance company that specializes in originating, underwriting, funding, servicing, and managing a portfolio of short-term (i.e., three years or less) loans secured by first mortgage liens on real property located primarily in Connecticut.

Each of Sachem’s loans is personally guaranteed by the principal(s) of the borrower, which is typically collaterally secured by a pledge of the guarantor’s interest in the borrower. Sachem generates around $65 million in total revenues.

Source: Investor Presentation

On August 14th, 2024, Sachem Capital posted its Q2 results for the period ending June 30th, 2024. Total revenues for the quarter came in at $15.2 million, down 7% compared to Q2-2023.

The decrease in interest income was due to lower number of loans originated, modified or extended in compared to last year. As a result, fee income from loans, primarily made up of origination fees, were down about 37.2% year-over-year.

Click here to download our most recent Sure Analysis report on SACH (preview of page 1 of 3 shown below):

High-Yield REIT No. 8: Annaly Capital (NLY)

- Dividend Yield: 13.4%

Annaly Capital Management invests in residential and commercial assets. The trust invests in various types of agency mortgage-backed securities, non-agency residential mortgage assets, and residential mortgage loans.

It also originates and invests in commercial mortgage loans, securities, and other commercial real estate investments.

On July 24, 2024, Annaly announced its financial results for the quarter ending June 30, 2024. The company reported a GAAP net loss of $0.09 per average common share, while earnings available for distribution (EAD) were $0.68 per average common share for the quarter. The company achieved an economic return of 0.9% for the second quarter and 5.7% for the first half of 2024.

Book value per common share at the end of the quarter was $19.25. Annaly’s GAAP leverage ratio increased to 7.1x, up from 6.7x in the prior quarter, while economic leverage rose to 5.8x from 5.6x. The company declared a quarterly common stock cash dividend of $0.65 per share.

Annaly’s total investment portfolio was valued at $74.8 billion, with $66.0 billion invested in a highly liquid Agency portfolio.

Click here to download our most recent Sure Analysis report on NLY (preview of page 1 of 3 shown below):

High-Yield REIT No. 7: New York Mortgage REIT (NYMT)

- Dividend Yield: 14.1%

New York Mortgage Trust acquires, invests in, finances, and manages mortgage-related assets and other financial assets. The trust doesn’t own physical real estate, but rather seeks to manage a portfolio of investments that are real estate related.

The trust invests in residential mortgage loans, multi family CMBS, preferred equity, and joint venture equity.

NYMT posted second quarter earnings on July 31st, 2024, and results were quite weak once again. Adjusted earnings-per-share came to a loss of 25 cents, which missed estimates for a profit of a dime by 35 cents. Total net interest income was $19.04 million, which was up 26% year-over-year, but still missed estimates by over $4 million.

Management noted that recent interest rate market activity was indicative of falling inflation and a slowing economy, with the two-year Treasury falling 29 basis points from its 2024 peak.

Click here to download our most recent Sure Analysis report on NYMT (preview of page 1 of 3 shown below):

High-Yield REIT No. 6: Two Harbors Investment Corp. (TWO)

- Dividend Yield: 14.1%

Two Harbors Investment Corp. is a residential mortgage real estate investment trust (mREIT). As such, it focuses on residential mortgage-backed securities (RMBS), residential mortgage loans, mortgage servicing rights, and commercial real estate.

The trust derives nearly all of its revenue in the form of interest through available-for-sale securities.

Two Harbors Investment Corp. (TWO) reported its second-quarter 2024 financial results, showing earnings per share (EPS) of $0.17, missing estimates by $0.27. Revenue for the quarter was -$38.25 million, down 8.48% year-over-year, missing expectations by $328,000.

Despite the challenging market conditions, the company delivered stable results, maintaining a book value of $15.19 per common share and declaring a second-quarter common stock dividend of $0.45 per share. For the first six months of 2024, Two Harbors generated a 5.8% total economic return on book value.

The company generated comprehensive income of $0.5 million, or $0.00 per weighted average basic common share, and repurchased $10.0 million in convertible senior notes due 2026.

Click here to download our most recent Sure Analysis report on TWO (preview of page 1 of 3 shown below):

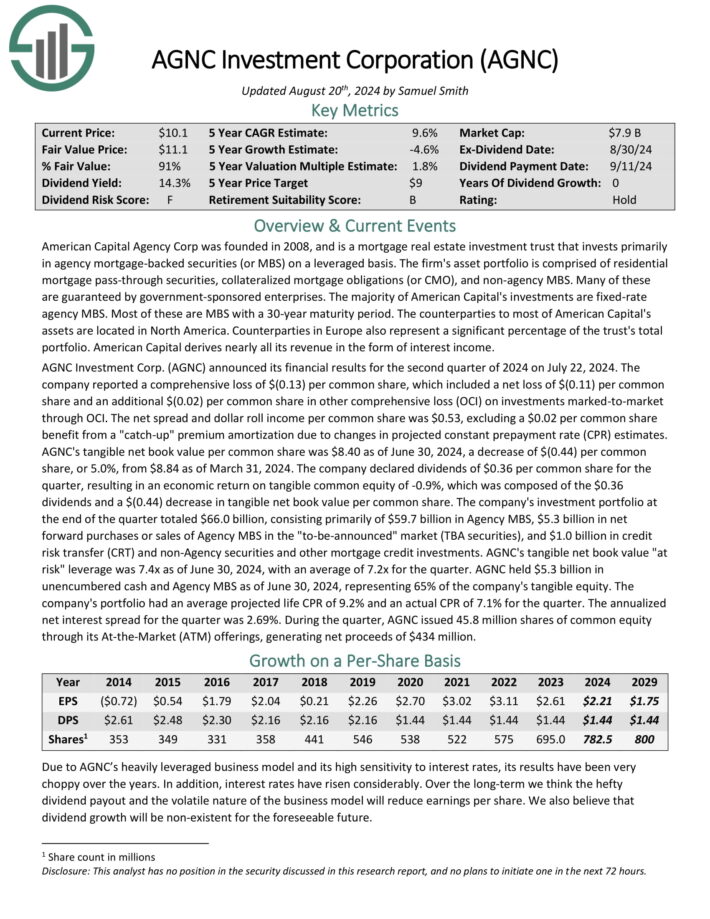

High-Yield REIT No. 5: AGNC Investment Corp. (AGNC)

- Dividend Yield: 14.2%

American Capital Agency Corp is a mortgage real estate investment trust that invests primarily in agency mortgage–backed securities (or MBS) on a leveraged basis.

The firm’s asset portfolio is comprised of residential mortgage pass–through securities, collateralized mortgage obligations (or CMO), and non–agency MBS. Many of these are guaranteed by government–sponsored enterprises.

AGNC Investment Corp. (AGNC) announced its financial results for the second quarter of 2024 on July 22, 2024. The company reported a comprehensive loss of $(0.13) per common share, which included a net loss of $(0.11) per common share and an additional $(0.02) per common share in other comprehensive loss (OCI) on investments marked-to market through OCI.

The net spread and dollar roll income per common share was $0.53, excluding a $0.02 per common share benefit from a “catch-up” premium amortization due to changes in projected constant prepayment rate (CPR) estimates.

AGNC’s tangible net book value per common share was $8.40 as of June 30, 2024, a decrease of $(0.44) per common share, or 5.0%, from $8.84 as of March 31, 2024.

Click here to download our most recent Sure Analysis report on AGNC Investment Corp (AGNC) (preview of page 1 of 3 shown below):

High-Yield REIT No. 4: Ellington Credit Co. (EARN)

- Dividend Yield: 14.3%

Ellington Credit Co. acquires, invests in, and manages residential mortgage and real estate related assets. Ellington focuses primarily on residential mortgage-backed securities, specifically those backed by a U.S. Government agency or U.S. government–sponsored enterprise.

Agency MBS are created and backed by government agencies or enterprises, while non-agency MBS are not guaranteed by the government.

On August 12th, 2024, Ellington Residential reported its second quarter results for the period ending June 30th, 2024. The company generated a net loss of $(0.8) million, or $(0.04) per share.

Ellington achieved adjusted distributable earnings of $7.3 million in the quarter, leading to adjusted earnings of $0.36 per share, which covered the dividend paid in the period.

Ellington’s net interest margin was 4.24% overall. At quarter end, Ellington had $118.8 million of cash and cash equivalents, and $44 million of other unencumbered assets.

Click here to download our most recent Sure Analysis report on EARN (preview of page 1 of 3 shown below):

High-Yield REIT No. 3: ARMOUR Residential REIT (ARR)

- Dividend Yield: 14.8%

ARMOUR Residential invests in residential mortgage-backed securities that include U.S. Government-sponsored entities (GSE) such as Fannie Mae and Freddie Mac.

It also includes Ginnie Mae, the Government National Mortgage Administration’s issued or guaranteed securities backed by fixed-rate, hybrid adjustable-rate, and adjustable-rate home loans.

Unsecured notes and bonds issued by the GSE and the US Treasury, money market instruments, and non-GSE or government agency-backed securities are examples of other types of investments.

ARR reported its unaudited second-quarter 2024 financial results and financial position as of June 30, 2024. The company announced a GAAP net loss related to common stockholders of $(51.3) million or $(1.05) per common share.

The company generated net interest income of $7.0 million and distributable earnings available to common stockholders of $52.5 million, equating to $1.08 per common share.

ARMOUR paid common stock dividends of $0.24 per share per month, totaling $0.72 per share for the second quarter. The average interest income on interest-earning assets was 5.00%, while the interest cost on average interest-bearing liabilities was 5.52%. The economic interest income was 4.74%, with an economic net interest spread of 2.05%.

Click here to download our most recent Sure Analysis report on ARMOUR Residential REIT Inc (ARR) (preview of page 1 of 3 shown below):

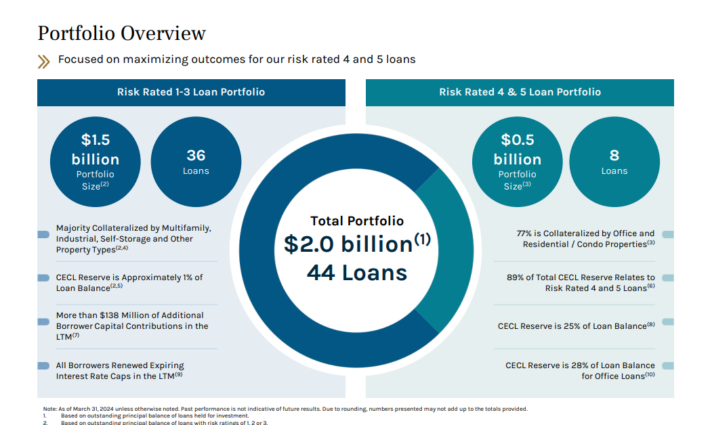

High-Yield REIT No. 2: Ares Commercial Real Estate (ACRE)

- Dividend Yield: 15.1%

Ares Commercial Real Estate Corporation is a specialty finance company primarily engaged in originating and investing in commercial real estate (“CRE”) loans and related investments. ACRE generated around $198.6 million in interest income last year.

The company’s loan portfolio (98% of which are senior loans) comprises 44 market loans across 8 asset types, with an outstanding principal balance of $2 billion. The majority of the loans are tied to multifamily, office, and mixed-use properties.

Source: Investor Presentation

In terms of geographical diversification, ACRE’s exposure features a healthy mix between the Southeast, West, and Midwest.

On August 6th, 2024, ACRE reported its Q2 results for the period ending June 30th, 2024. Interest income came in at $40.8 million, 21% lower year-over-year.

The decline was due to the company’s loans struggling to perform as higher rates of inflation and certain cultural shifts such as work-from-home trends continue to impact the operating performance and the economic values of commercial real estate.

In the meantime, interest expense rose by 2% to about $27.5 million. Thus, total revenues (interest income – interest expenses + $3.43 million in revenue from ACRE’s own real estate) fell by 33% to roughly $16.8 million.

Click here to download our most recent Sure Analysis report on ACRE (preview of page 1 of 3 shown below):

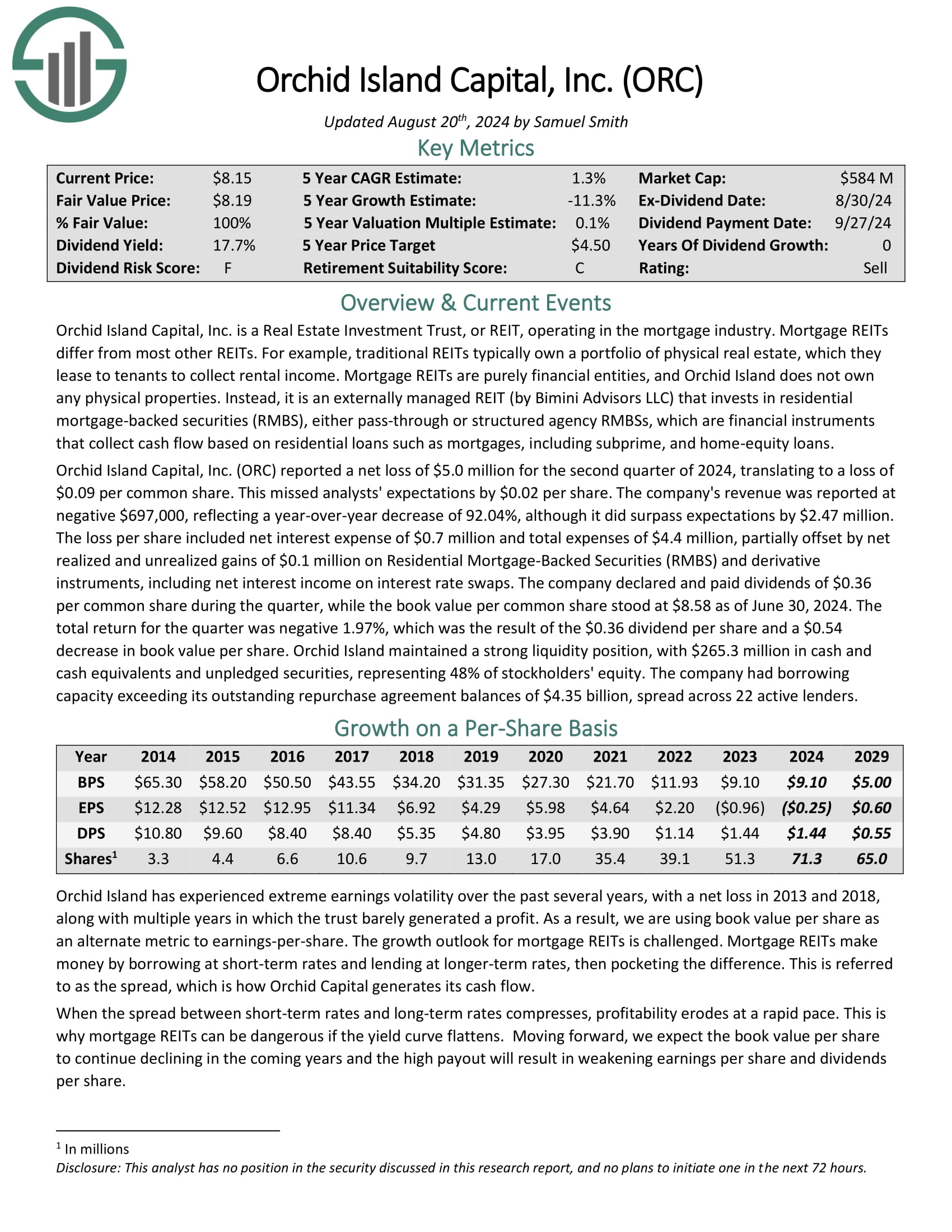

High-Yield REIT No. 1: Orchid Island Capital Inc (ORC)

- Dividend Yield: 18.6%

Orchid Island Capital is a mortgage REIT that is externally managed by Bimini Advisors LLC and focuses on investing in residential mortgage-backed securities (RMBS), including pass-through and structured agency RMBSs.

These financial instruments generate cash flow based on residential loans such as mortgages, subprime, and home-equity loans.

Orchid Island reported a net loss of $5.0 million for the second quarter of 2024, translating to a loss of $0.09 per common share. This missed analysts’ expectations by $0.02 per share. The company’s revenue was reported at negative $697,000, reflecting a year-over-year decrease of 92.04%, although it did surpass expectations by $2.47 million.

The loss per share included net interest expense of $0.7 million and total expenses of $4.4 million, partially offset by net realized and unrealized gains of $0.1 million on Residential Mortgage-Backed Securities (RMBS) and derivative instruments, including net interest income on interest rate swaps.

The company declared and paid dividends of $0.36 per common share during the quarter, while the book value per common share stood at $8.58 as of June 30, 2024.

Click here to download our most recent Sure Analysis report on Orchid Island Capital, Inc. (ORC) (preview of page 1 of 3 shown below):

Final Thoughts

REITs have significant appeal for income investors due to their high yields. These 10 extremely high-yielding REITs are especially attractive on the surface, although investors should be aware that abnormally high yields are often accompanied by elevated risks.

If you are interested in finding high-quality dividend growth stocks and/or other high-yield securities and income securities, the following Sure Dividend resources will be useful:

High-Yield Individual Security Research

Other Sure Dividend Resources

- Dividend Kings: 50+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Monthly Dividend Stocks: Individual securities that pay out every month