Updated on November 4th, 2024 by Aristofanis Papadatos

The Dividend Kings are an illustrious group of companies. These companies stand apart from the vast majority of the market as they have raised dividends for at least 50 consecutive years.

We believe that investors should view the Dividend Kings as the most high-quality dividend growth stocks to buy for the long term.

With this in mind, we created a full list of all the Dividend Kings.

You can download the full list, along with important financial metrics such as dividend yields and price-to-earnings ratios, by clicking the link below:

This group is so exclusive that there are just 53 companies that qualify as a Dividend King. Fortis Inc. (FTS) recently raised its dividend for the 51st consecutive year, joining the list of Dividend Kings.

This article will discuss the company’s business overview, growth prospects, competitive advantages, and expected returns.

Business Overview

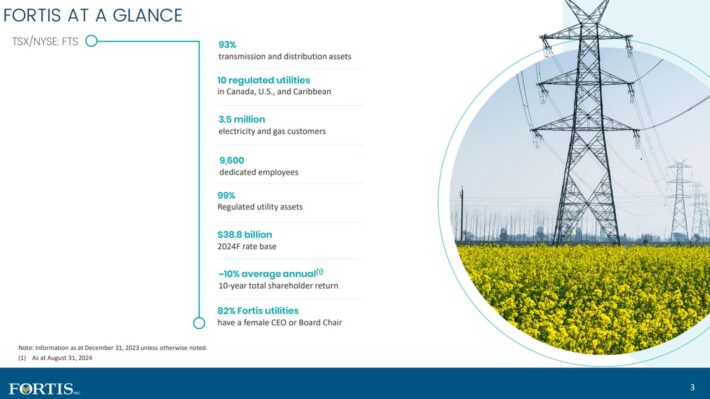

Fortis is Canada’s largest investor-owned utility business with operations in Canada, the United States, and the Caribbean. It is cross-listed in Toronto and New York.

Fortis trades with a current after-tax yield of 3.7% (about 4.3% before the 15% withholding tax applied by the Canadian government). Unless otherwise noted, US$ is used in this research report.

Fortis currently has 99% regulated assets: 82% regulated electric and 17% regulated gas. Approximately 64% are in the U.S., 33% in Canada, and 3% in the Caribbean.

Source: Investor Presentation

Fortis reported Q2 2024 results on 07/31/24. The company reported adjusted earnings per share (EPS) were up 8%.

The year-to-date results provide a bigger picture. Over this period, Fortis grew adjusted earnings by 7%, while the adjusted earnings per share were up 5%.

The utility’s 2024 capital plan of CAD$4.8 billion (roughly $3.4 billion in U.S. dollars) is on track, with nearly half invested in the first six months of 2024. We expect Fortis to post earnings per share of about US$2.34 in the full year.

The increase in earnings in the third quarter was driven by strong earnings in Arizona, reflecting new customer rates at Tucson Electric Power and higher retail electricity sales associated with warmer weather.

Rate base growth across utilities and the timing of recognition of new cost of capital parameters approved in 2023 also contributed to earnings growth.”

Notably, Fortis raised its quarterly dividend by 6% in September.

Growth Prospects

Utility companies are typically classified as slow, but steady growers. Indeed, we expect Fortis to grow its earnings-per-share by 5.5% annually over the next five years. This growth will be driven by multiple factors.

After releasing its five-year capital plan of CAD$26 billion (roughly $18.7 billion in U.S. dollars) for 2025 to 2029, which suggests a mid-year rate base growth at a compound annual growth rate of ~6.5%. The company also maintained its dividend growth guidance of 4%-6% through 2029.

Source: Investor Presentation

The capital plan includes investing in areas, such as a greener and improved grid and a shift from fossil fuel to solar and wind generation. Importantly, this growth rate is before the impact of acquisitions, which have historically been important for Fortis.

Competitive Advantages & Recession Performance

Utility companies often benefit from multiple advantages. The first is that they usually operate in a near-monopoly on the areas that they service.

Because demand for Fortis’s utility services doesn’t change much in various economic environments, Fortis’s results have been quite resilient through economic uncertainties, including the one we’re experiencing in which inflation and interest rates are higher than recent history.

In addition, Fortis is unique because of its cross-border exposure. Its timely U.S. acquisitions of regulated utilities since 2013 have allowed Fortis to now generate more than half of its revenue from that country.

Given these built-in advantages, many utilities often outperform other sectors of the market during recessions. Below are the company’s earnings-per-share results during, and after, the Great Recession:

- 2007 earnings-per-share: $1.32

- 2008 earnings-per-share: $1.52 (15% increase)

- 2009 earnings-per-share: $1.51 (~1% decrease)

- 2010 earnings-per-share: $1.81 (20% increase)

The company grew its diluted earnings-per-share in 2008, followed by just a minor decline in 2009, which was the worst year of the recession. Fortis then quickly rebounded with 20% earnings growth in 2010.

Valuation & Expected Total Returns

We expect Fortis to generate earnings-per-share of US$2.34 in 2024. At the current share price, FTS stock trades for a price-to-earnings ratio of 18.2.

Given the company’s stable business model, we believe fair value is 19 times earnings, which is close to the average valuation of the stock for the last five years.

Reverting to our target valuation by 2029 would result in a multiple expansion, boosting annual returns by 0.9%. In addition, we expect annual EPS growth of 5.5% which will also contribute to shareholder returns.

Finally, dividends will boost returns as FTS stock currently yields 4.3%.

Source: Investor Presentation

FTS has now raised its dividend for 51 consecutive years. Fortis’ payout ratio has traditionally been about 70% of earnings. The dividend is important to management, and we believe it is safe and should continue to rise for years to come.

Therefore, FTS is expected to return 10.1% per year on average through 2029. An expected return above 10% qualifies FTS stock as a buy.

Final Thoughts

There is much to like about Fortis, such as its recession-proof business model, the high success of rate increase approvals, and the long history of dividend growth. Only the most well-run businesses can pay dividends for as long as Fortis has.

Shares of Fortis appear reasonably valued. The company should continue to grow earnings, and consequently its dividends, for many years. With an expected return slightly above 10%, the stock is a buy.

Additional Reading

The following articles contain stocks with very long dividend or corporate histories, ripe for selection for dividend growth investors:

- The High Yield Dividend Aristocrats List is comprised of the 20 Dividend Aristocrats with the highest current yields.

- The Dividend Achievers List is comprised of ~350 stocks with 10+ years of consecutive dividend increases.

- The High Yield Dividend Kings List is comprised of the 20 Dividend Kings with the highest current yields.

- The Blue Chip Stocks List: stocks that qualify as Dividend Achievers, Dividend Aristocrats, and/or Dividend Kings

- The High Dividend Stocks List: stocks that appeal to investors interested in the highest yields of 5% or more.

- The Monthly Dividend Stocks List: stocks that pay dividends every month, for 12 dividend payments per year.

- The Dividend Champions List: stocks that have increased their dividends for 25+ consecutive years.

Note: Not all Dividend Champions are Dividend Aristocrats because Dividend Aristocrats have additional requirements like being in The S&P 500. - The Dividend Contenders List: 10-24 consecutive years of dividend increases.

- The Dividend Challengers List: 5-9 consecutive years of dividend increases.

- The Complete List of Russell 2000 Stocks

- The Complete List of NASDAQ-100 Stocks